June 29, 2026

Re: H.R. 5775, the FCRA Liability Harmonization Act (Loudermilk)(oppose)

H.R. 8141, the Fair Credit Reporting Reseller Accuracy Act (Lawler)(oppose)

Dear Representative:

The undersigned 38 consumer and advocacy groups write to you to express opposition to H.R. 5775, the FCRA Liability Harmonization Act (Loudermilk) and H.R. 8141, the Fair Credit Reporting Reseller

Accuracy Act (Lawler). In short:

H.R. 5775, the FCRA Liability Harmonization Act, would dramatically reduce accountability for credit bureaus and other companies, including when they wrongfully label innocent consumers as bad borrowers or criminals. The bill eliminates punitive damages under the Fair Credit Reporting Act (FCRA), no matter how egregious the violation. It caps both statutory damages and actual damages for class actions to $500,000, no matter how many thousands or millions of consumers were harmed or the extent of their losses caused by illegal conduct. It also caps attorney’s fees, no matter how complicated the case or obstructionist the defense counsel, gutting the fee shifting nature of the Act, an essential part of the Act’s enforcement/ accountability framework, and a common tool across the American legal landscape.

H.R. 8141, the Fair Credit Reporting Reseller Accuracy Act, purports to impose new accuracy standards on resellers, companies that assemble and merge information from other consumer reporting agencies, but it actually instead gives these companies a free pass from liability. Resellers would be off the hook for errors if they conveyed information unaltered from another company, even if the inaccuracy was obvious on its face, such as facially illogical or contradictory information, or the other company has a history of problems. Many resellers are multi-billion-dollar companies (some owned by private equity), with more than adequate resources for compliance.

A. H.R. 5775, the “FCRA Liability Harmonization Act,” would dramatically reduce accountability for credit bureaus and other companies

H.R. 5775 drastically decreases the consequences for credit bureaus, employment background check agencies, tenant screeners and other “consumer reporting agencies” (CRAs) when they violate the FCRA, including when they falsely claim that consumers have failed to pay their bills or have criminal records. The bill would eliminate punitive damages, both in class actions and in individual cases, for willful violations of the FCRA, no matter how egregious the conduct. It would impose an arbitrary, one-size-fits-all cap on both statutory damages and actual damages for class actions to $500,000, no matter how many thousands or millions of consumers were harmed or the extent of their losses caused by the illegal conduct.

H.R. 5775 radically reduces accountability for the most serious violations that these Big Data companies commit. It also does the same for the banks, lenders, and debt collectors (known as “furnishers” under the FCRA) when they supply false information to these companies and then fail to correct it. Being falsely accused of skipping bills or committing a crime is not only upsetting and distressing, it can deprive individuals of their ability to access credit, employment, rental housing and more.

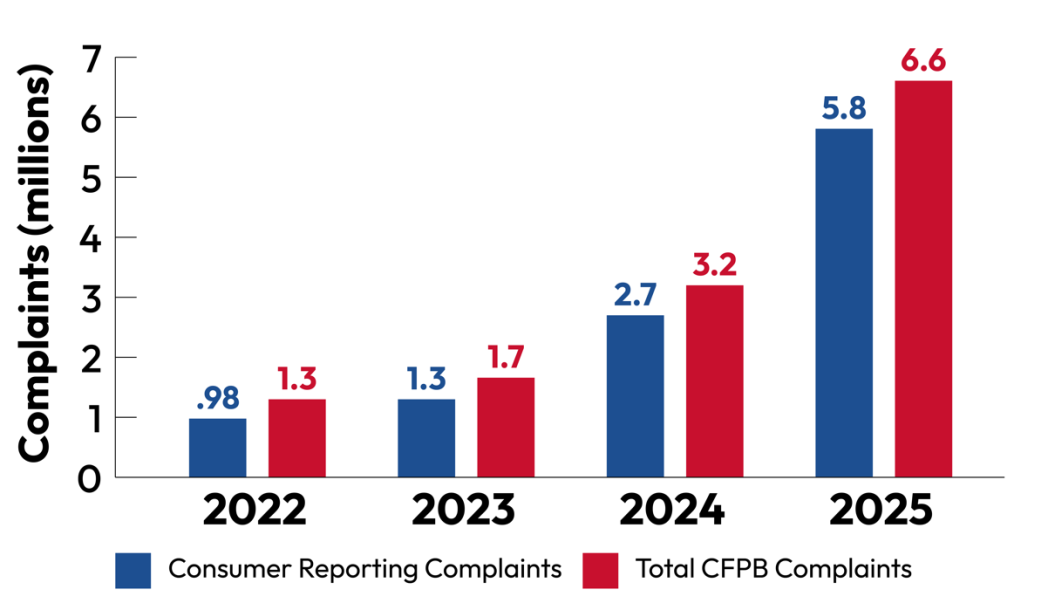

- H.R. 5775 is a boondoggle for the most-complained about companies in financial services, with over 5 million CFPB complaints against them last year

This bill is a giveaway to one of the most problematic sectors in the financial services industry. The three major credit bureaus (Equifax, Experian and TransUnion) and other CRAs have been by far the most complained-about companies to the CFPB for many years, with an eye-popping number of complaints against them for the past few years:

- 2022: 978,000 complaints1

- 2023: 1.3 million complaints.2

- 2024: 2.7 million complaints3

- 2025: 5.8 million complaints!4

As this chart shows, consumer reporting complaints make up the vast majority of complaints to the CFPB.

This massive volume of complaints is unsurprising given what we know of the credit bureaus’ dysfunction. As the Federal Trade Commission found,1 in 5 of consumers (or over 40 million) had verified errors in their credit reports, with 1 in 20 (or over 10 million) having errors so serious they would be rejected for credit or need to pay more.5 More recent studies by Consumer Reports in 20216 and 20247 show similar percentages.

These high error levels are the result of deep, profound, and longstanding problems in the credit reporting system, such as consumers having their credit files “mixed” with the wrong person, the after-effects of identity theft, and consumers being labeled as dead when they are alive and breathing.8 The dispute system that is supposed to serve as a safety net to fix errors is an automated travesty, with the Big Three credit bureaus and some furnishers conducting pro forma, perfunctory investigations. Credit bureaus automatically defer to what a furnisher tells them, like a judge who always rules for the defendant.9

- Abuses by credit bureaus, background check agencies, and tenant screeners shut people out of jobs, opportunity, and housing, sometimes even resulting in homelessness and irreversible tragedies

Credit bureaus, employment background check agencies, tenant screeners, big banks, and debt collectors inflict real and serious harm on people when they report inaccurate information, and should be subject to punitive damages. For example:

- In Taylor v. Equifax, Equifax mixed the credit report of plaintiff David Anthony Taylor with David Allan Taylor, despite a different social security number and date of birth, with devastating results for David Anthony Taylor. Taylor, a veteran, had put his house on the market after having been preapproved for a VA home mortgage and found a new home. But he was unable to close on his new home, because Equifax had added numerous negative accounts from David Allen Taylor. David Anthony Taylor disputed the inaccurate information several times over the course of six months but Equifax failed to fix its mistakes. Unable to close on his new home, and having sold his old home, Taylor had nowhere to live and could not find an apartment that would accept his pit bulls. Taylor ultimately spent months in a motel, was forced to kennel board and re-home a number of his dogs, and even had to put two dogs to sleep because he could not find somewhere to re-home them.10

- In Cornelius v. Samba Security, an Uber driver had her account deactivated because a background check CRA falsely reported that her driver’s license had been withdrawn. Cornelius disputed this inaccurate reporting twice, including a copy of her valid driver’s license, but SambaSafety failed to correct it. In conducting its alleged investigation, SambaSafety failed to even contact the state Department of Motor Vehicles. SambaSafety’s incompetence resulted in Cornelius losing 13 months of income, including approximately $7,000 per month during the height of Alaska’s summer tourist season. A jury awarded Cornelius both actual damages and punitive damages for Samba Security’s failure to correct an obvious error that was easily fixable.11

- In Cayler v. TransUnion Rental Screening Solutions, Inc., a subsidiary of TransUnion issued an inaccurate tenant screening report falsely claiming that Cayler was convicted of “Indecency with a Child Sexual Contact” and “Indecency with a Child by Contact.” The potential landlord rejected his rental application, only relenting after the plaintiff explained the situation directly and requiring him to pay six months rent in advance, totaling over $18,000. Cayler was understandably deeply distressed by TransUnion’s false labeling of him as a child sex offender and his having to prove his innocence to a prospective landlord.12

Additional case examples of significant harm from inaccurate information are included in NCLC’s testimony from an April 16, 2026 Subcommittee on Financial Institutions hearing,13 as well as a September 2017 hearing on the previous version of this bill.14

- H.R. 5775’s severe cutbacks in liability would reduce the FCRA’s remedies far below other consumer laws and prevent accountability for widespread systemic failures such as the Equifax data breach

H.R. 5775 would deny all of the consumers discussed above the ability to seek full accountability for the outrageous violations of the FCRA that affected their lives. In addition to eliminating punitive damages and capping class action damages at $500,000, the bill limits attorney’s fees to the lesser of 40% of the damages recovery or $100,000. This cap would apply no matter how complicated the case, including class actions involving millions of class members such as the Equifax data breach.15 It would decimate the fee-shifting nature of the FCRA, devastating the ability of injured consumers to seek legal assistance. And it would give enormous incentive for industry attorneys to obstruct, delay, and drag out litigation, knowing that consumer attorneys would have their fees capped no matter how badly industry attorneys behaved. H.R. 5775 purports to merely “harmonize” the FCRA with other consumer laws, but no other consumer law limits attorney’s fees in this manner or caps actual damages in class actions to $500,000.

B. H.R. 8141, the “Fair Credit Reporting Reseller Accuracy Act,” lets resellers off the hook for liability over errors they should have detected

H.R. 8141 is framed as imposing new accuracy standards on resellers, but it actually would give these companies immunity over inaccuracies for which they should bear responsibility. Resellers are a specific type of consumer reporting agency (CRA) under the FCRA that “assembles and merges information” from one or more other CRAs.16 H.R. 8141 gives resellers a free pass from liability for inaccuracies if they are conveying from the other CRA, and is essentially a get-out-of-jail-free card.

- H.R. 8141 is a Trojan House bill that purports to add new consumer protections, but actually immunizes resellers from the FCRA’s accuracy requirement

H.R. 81841 is purported to help consumers and add a “new” requirement for resellers to have procedures to ensure “maximum possible accuracy.”17 But the vast majority of legal cases, such as the three examples discussed below, already apply this standard to resellers, which is contained in Section 1681e(b) of the FCRA.

More disturbingly, H.R. 8141 contains a “Limitation on Liability” provision in paragraph (2) that states, “No reseller may be held liable under this title if such reseller accurately communicates information obtained from another consumer reporting agency to an end user or another reseller.” This is a legal immunity provision for resellers, letting them off the hook if they are conveying information unaltered from another CRA.

- H.R. 8141 would immunize resellers when they ignore facially illogical or internally contradictory information, such as reporting a consumer as deceased even though the consumer can show they are living, or when resellers use information from unreliable sources

H.R. 8141 would let resellers off the hook even when the reseller knew or should have known that the information from the original CRA was inaccurate or questionable enough to have triggered a duty to investigate further. For instance, there are times when a reseller receives information from other CRAs that is internally contradictory or illogical, where they should have investigated further, not pass along this junk data. Examples include:

- In Ocasio v. CoreLogic Credco, L.L.C.,18 a reseller sold a consumer report that included negative information belonging to the plaintiff’s grandmother. The inaccuracy was obvious from the face of the consumer report because it included the accounts owned by individuals with different birth years (1938 vs. 1987), yet the reseller made no effort to resolve the inconsistency.

- In Oatway v. Experian Info. Sols., Inc.,19 a reseller communicated inaccurate information received from Experian that the consumer was deceased. The error was caused due to the entry of an incorrect Social Security number, which was the fault of either the reseller or the auto dealership. Regardless, the reseller had facially contradictory information as to the consumer’s death in its possession, i.e., that the consumer was making payments “on 35 total accounts and provided proof of his identity in person at the dealership” which should have provided notice to the reseller that there was a problem.

- In Rogue v. CoreLogic Credco, LLC,20 a reseller inaccurately reported that the consumer filed for bankruptcy. Only Equifax had reported the bankruptcy, TransUnion and Experian had not. The court held that the reseller could be held liable for the inaccuracy given this inconsistency between the information supplied by the three credit bureaus, and “specifically noted that other district courts have repeatedly rejected Credco’s and other resellers’ arguments that a reseller is only required to accurately reproduce the information furnished to it by other credit bureaus.“21

Note the CFPB had issued guidance stating that CRAs should have reasonable procedures to prevent the inclusion of the facially inconsistent and illogical information, such as an inaccurate “deceased” notation when every other tradeline is reporting ongoing payment activity.22 Resellers are already on notice that they need to investigate and resolve facially illogical information before issuing reports, even if that information comes from another CRA, including information that is inconsistent between the Big Three credit bureaus. This bill would undermine this requirement by letting resellers escape from liability in such circumstances, potentially increasing the amount of junk data. This harms both consumers as well as creditors who lose valuable information as to who would be a good customer.

Tenant screening CRAs are another type of reseller, which are used by landlords to determine whether or not to approve rental housing applications. One of the problems in tenant screening is the failure of CRAs to report information about the dispositions of eviction or criminal records, including dispositions favorable to the tenant. In Grant v RentGrow,23 the court held that a reseller could be held liable for reporting the filing of an eviction proceeding without reporting that the eviction had been dismissed in the plaintiff’s favor, even though the information originated from TransUnion’s tenant screening subsidiary, because RentGrow had warning signs that TransUnion might not be reliable.

- The reseller industry is dominated by multi-billion-dollar corporations, not mom-and-pop companies, with several large players owned by private equity

Many resellers are large multinational corporations, including private-equity owned companies, which have more than adequate resources to comply with these requirements, i.e., reconciling facially illogical information and making sure public record information is up to date. Resellers are sometimes portrayed as being small, family-owned businesses, but that is often not the case. One of the most prominent resellers is CoreLogic Credco, now known as Cotality. CoreLogic was formerly a publicly traded company that was purchased by a private equity fund for $6 billion and taken private in 2021,24hardly a mom-and-pop company unable to perform due diligence checks.

Another prominent provider of tri-merged credit reports is Equifax Mortgage Solutions.25 A third leading mortgage reseller is private equity-owned26 Xactus, which has over 6,500 clients ranging and 12 operation centers across the U.S.,27 and lists former House speaker Paul Ryan as a Board member.28

Many tenant screening CRAs, such as RentGrow, RealPage, SafeRent, and AppFolio are also not small family-owned businesses. RentGrow is owned by Yardi,29 which boasts “over 9,000 professionals in more than 40 offices worldwide.”30 RealPage, the company behind the notorious rent price-fixing algorithm,31 was acquired by private equity firm Thoma Bravo for $10.2 billion in April 2021.32

- H.R. 8141 would encourage CRAs to structure themselves as resellers to avoid FCRA liability

While not all tenant screening CRAs may currently consider themselves to be resellers currently, they certainly will be incentivized to do so if resellers are granted immunity from liability for inaccuracies under the FCRA. Other types of CRAs such as criminal background check CRAs, are likely to restructure themselves as resellers if they are granted immunity. This would likely lead to even more inaccuracies in a problematic industry that has such enormous impact on both workers and employers; an inaccurate employment background check could be devastating in costing a worker a much-needed job.

For these reasons, we urge you to vote NO on H.R. 5775, the FCRA Liability Harmonization Act and H.R. 8141, the Fair Credit Reporting Reseller Accuracy Act. Thank you for your attention. If you have any questions about this letter, please contact Chi Chi Wu ([email protected]) at (617) 226-0326.

National Organizations

National Consumer Law Center (on behalf of its low-income clients)

American Association for Justice (AAJ)

Americans for Financial Reform

Center For Responsible Lending

Center for Survivor Agency and Justice

Check My Ads Institute

Consumer Action

Consumer Federation of America

Consumer Reports

Electronic Privacy Information Center (EPIC)

JustLeadershipUSA

National Association of Consumer Advocates

National Community Reinvestment Coalition

National Consumers League

National Disability Institute

National Fair Housing Alliance

National Housing Law Project

PolicyLink

State and Local Organizations

Center for Economic Integrity (AZ)

Arkansas Community Organizations

The Academy of Financial Education (CA)

East Bay Community Law Center (CA)

Housing and Economic Rights Advocates (CA)

Public Law Center (CA)

Legal Aid DC

Jacksonville Area Legal Aid Inc. (FL)

Georgia Watch

Greater Boston Legal Services (MA)

Cambridge Economic Opportunity Committee (MA)

Northern Nevada Legal Aid

New Jersey Citizen Action

New Yorkers for Responsible Lending

Advocates for Basic Legal Equality Inc (OH)

Oregon Consumer League

Oregon Consumer Justice

South Carolina Appleseed Legal Justice Center

Texas Appleseed

Legal Aid Works (VA)

Endnotes

- CFPB, Consumer Response Annual Report January 1–December 31, 2022 3, 11 (Mar. 2023), https://www.consumerfinance.gov/data-research/research-reports/2022-consumer-response-annual-report/. ↩

- CFPB, Consumer Response Annual Report January 1-December 31, 2023, at 11, 19 (Mar. 2024), https://files.consumerfinance.gov/f/documents/cfpb_cr-annual-report_2023-03.pdf. ↩

- CFPB, Consumer Response Annual Report January 1-December 31, 2024, at 3, 11 (May 2025), https://files.consumerfinance.gov/f/documents/cfpb_cr-annual-report_2025-05.pdf. ↩

- CFPB, Consumer Response Annual Report January 1-December 31, 2025, at 7 (March 2026), https://www.consumerfinance.gov/data-research/research-reports/2025-consumer-response-annual-report/. ↩

- Fed. Trade Comm’n, Report to Congress Under Section 319 of the Fair and Accurate Credit Transactions Act of ↩

- Syed Ejaz, Consumer Reports, A Broken System: How the Credit Reporting System Fails Consumers and What to Do About It (2021) https://advocacy.consumerreports.org/wp-content/uploads/2021/06/A-Broken-System-How-the-Credit-Reporting-System-Fails-Consumers-and-What-to-Do-About-It.pdf. ↩

- Lisa L. Gill, Consumer Reports, More Than a Quarter of People Find Serious Mistakes in Their Credit Reports, Study Shows (April 30, 2024), https://www.consumerreports.org/money/credit-scores-reports/serious-mistakes-found-in-credit-reports-a1061511185/. ↩

- Chi Chi Wu, Michael Best & Sarah Mancini, NCLC, Automated Injustice Redux: Ten Years after a Key Report, Consumers Are Still Frustrated Trying to Fix Credit Reporting Errors (Feb. 25, 2019), https://bit.ly/ajustre. See also Consumer Credit Reporting: Assessing Accuracy and Compliance: Hearing Before the Subcomm. on Oversight and Investigations of the H. Comm. on Financial Servs., 117th Cong. (2021) (statement of Chi Chi Wu), https://www.congress.gov/117/meeting/house/112712/witnesses/HHRG-117-BA09-Wstate-WuC-20210526.pdf. ↩

- Id. ↩

- Amended Complaint, Taylor v. Equifax Info. Serv., Case No. 8:23-cv-00860 (M.D. Fla. March 18, 2024), https://storage.courtlistener.com/recap/gov.uscourts.flmd.413266/gov.uscourts.flmd.413266.46.0.pdf ↩

- Complaint, Cornelius v. Safety Holdings, Inc., Civ. No. 24-0811 (D.N.M. Aug. 14, 2024), https://storage.courtlistener.com/recap/gov.uscourts.nmd.505497/gov.uscourts.nmd.505497.1.0_1.pdf. ↩

- Cayler v. TransUnion Rental Screening Solutions, Inc., Case. No. 8:23-cv-01170 (M.D. Fla. May 26, 2023), https://storage.courtlistener.com/recap/gov.uscourts.flmd.414573/gov.uscourts.flmd.414573.1.0.pdf ↩

- Promoting Access to Credit for Everyday Americans : Hearing Before the Subcomm. on Fin. Inst. of the H. Comm. on Financial Servs., 119th Cong. (2026) (statement of Chi Chi Wu), https://www.nclc.org/resources/testimony-before-the-subcommittee-on-financial-institutions-of-the-house-financial-services-committee-opposing-harmful-fair-credit-reporting-act-amendments/ ↩

- Legislative Proposals for a More Efficient Federal Financial Regulatory Regime: Hearing Before the Subcomm. on Fin. Inst. and Consumer Credit of the H. Comm. on Financial Servs., 115th Cong. (2017) (statement of Chi Chi Wu), https://financialservices.house.gov/uploadedfiles/hhrg-115-ba15-wstate-ccwu-20170907.pdf. ↩

- The Equifax data breach, where hackers stole the private personal information of 147 million Americans due to that company’s lax security measures, resulted in a $380.5 million settlement for injured consumers. Peter Hayes, Equifax to Pay $380.5 Million to Settle Data Breach Class Claims, Bloomberg News, Jan. 14, 2020, https://news.bloomberglaw.com/product-liability-and-toxics-law/equifax-to-pay-380-5-million-to-settle-data-breach-class-claims.Ironically,thelasttimethatabillcalledthe “FCRA Liability Harmonization Act,”” was discussed in this Subcommittee was at a September 7, 2017 hearing – the same day that the Equifax data breach was publicly revealed. ↩

- U.S.C. § 1681a(u). ↩

- Press Release, Lawler, Gottheimer Introduce Bipartisan Bill to Strengthen Credit Data Accuracy and Protect Consumers, Mar. 30, 2026, https://lawler.house.gov/news/documentsingle.aspx?DocumentID=5718 ↩

- WL 5722828, (D.N.J. Sept. 29, 2015). ↩

- WL 2689029 (W.D. Wash. Sept. 19, 2025) ↩

- WL 7061745 (D. Idaho Dec. 2, 2020) ↩

- Id. at 4. ↩

- CFPB, Advisory Opinion on Fair Credit Reporting; Facially False Data (Oct. 20, 2022), available at https://files.consumerfinance.gov/f/documents/cfpb_fair-credit-reporting-facially-false-data_advisory-opinion_2022-10.pdf. ↩

- WL 5813140 (W.D. Tex. Sept. 6, 2023). ↩

- CoreLogic to be acquired by PE firms for $6bn, Financier Worldwide Magazine, April 2021, https://www.financierworldwide.com/corelogic-to-be-acquired-by-pe-firms-for-6bn. ↩

- Equifax, Equifax Mortgage Merged Credit Report, 2025, https://assets.equifax.com/marketing/US/assets/mortgage-merged-credit-report.pdf ↩

- One of Xactus’s owners is private equity firm Lovell Minnick. Press Release, UniversalCIS Announces Investment from Lovell Minnick Partners, Mar. 17, 2021, https://xactus.com/universalcis-announces-investment-from-lovell-minnick-partners/ ↩

- Xactus, Xactus Named One of America’s Fastest-Growing Companies, https://xactus.com/inc-5000-named-xactus-no-288-among-americas-fastest-growing-private-companies/ (viewed April 12, 2026). ↩

- Xactus, About Us, https://xactus.com/about/ (viewed April 12, 2025). ↩

- CFPB, List of Consumer Reporting Companies, at 23, https://files.consumerfinance.gov/f/documents/cfpb_consumer-reporting-companies_list_2025.pdf ↩

- Yardi, About Us, https://www.yardi.com/company/about-us/ (viewed April 12, 2025). ↩

- Heather Vogell, Rent Going Up? One Company’s Algorithm Could Be Why, ProPublica, Oct. 15, 2022, https://www.propublica.org/article/yieldstar-rent-increase-realpage-rent. ↩

- RealPage, Thoma Bravo Completes Acquisition of RealPage, April 22, 2021, https://www.realpage.com/news/thoma-bravo-completes-acquisition-of-realpage/. ↩